When shipping internationally, one field on the commercial invoice causes more confusion—and penalties—than any other: The Declared Value.

This figure, combined with your HS Classification, is the mathematical basis for your import duty. Over-declare, and you burn cash on unnecessary taxes. Under-declare, and you risk audit, seizure, and legal action.

What You Will Learn in This Guide

Methodology

- Transaction value vs. fallback methods

- Logistics: How Incoterms affect duty

Strategy

- Wholesale vs. Retail valuation

- Compliance: Avoiding "First Sale" traps

The Three Pillars of Duty Assessment

Customs agencies (like the CBSA in Canada or CBP in the USA) calculate duty based on a specific formula involving three data points:

- Declared Value: The monetary worth assigned to the goods.

- Country of Origin: Where the goods were actually made (not just shipped from).

- HS Code: The tariff classification number. Learn about HS Codes here.

Please feel free to send us your shipment details for our lowest spot quote

- Pickup location

- Delivery location

- Commodity, Weight and dimensions

- Cargo ready date

- Preferred mode of transport (Air / Ocean/ground )

- Required Incoterm

Method 1: Transaction Value

The Transaction Value is the primary method used by the World Trade Organization (WTO). It is defined as the price actually paid or payable for the goods when sold for export to the country of importation.

However, "Price Paid" is not always the final number. You must adjust for:

- Additions: Packing costs, selling commissions, assists (tools or molds provided by the buyer), and royalties.

- Deductions: Construction or maintenance costs after importation, and duties or taxes already included in the price.

If you are shipping a warranty replacement or a free sample, the transaction value is not zero. You must declare the fair market value—what the item would cost if you sold it. Always mark the invoice: "Value for Customs Purposes Only - No Commercial Charge."

Need Help with Customs Valuation?

Our experts provide personalized support to ensure your shipments are classified correctly and compliant.

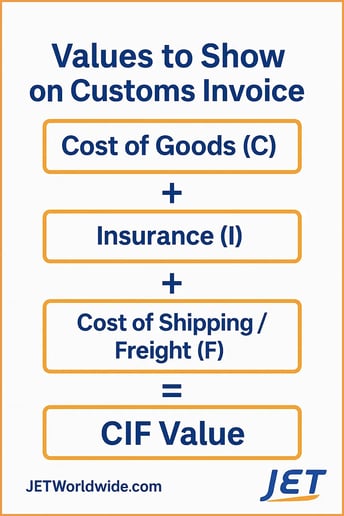

The Difference Between CIF and FOB

Crucially, different countries determine the "Value for Duty" differently regarding shipping costs. This distinction can significantly alter your landed cost.

| Valuation Method | What is Included? | Primary Regions |

|---|---|---|

| FOB (Free on Board) | Cost of Goods + Export Packing | USA, Australia |

| CIF (Cost, Insurance, Freight) | Cost of Goods + Export Packing + Shipping and Insurance | Canada, Europe, UK |

Example: If you ship a $1,000 laptop to Canada (CIF) with a $100 shipping cost, the GST and Duty are calculated on $1,100. If that same laptop goes to the USA (FOB), duty is calculated on $1,000.

The Great Divide: Transaction Value vs. The "No Sale" Valuation

In the world of business valuation, there is often a massive disconnect between what a business owner thinks their company is worth and what a valuation report says it is worth. This confusion usually stems from mixing up two distinct concepts: Transaction Value and "No Sale" Valuation.

To make smart decisions, you must understand whether you are looking at a real-world deal or a hypothetical model.

1. Transaction Value: The "Real World" Price

Transaction value is the specific price paid in an actual deal between a specific buyer and a specific seller. It is messy, human, and influenced by unique circumstances.

When the Invoice Isn't the Whole Customs Value

The general rules for customs valuation are largely harmonized globally drawing from the WTO Valuation Agreement. The key differentiator between jurisdictions is often whether transportation cost and insurance are considered part of the declared value. Most often referred to as the CIF value.

- The cost of shipping and insurance is considered part of the transaction value and most countries most countries including Canada and the EU.

- Some countries considered shipping as part of the transaction value, but not insurance

- The United States does not consider transport and insurance cost as part of the transaction value

What does not vary most major customs regulations,is the principle that the declared value must reflect the full economic transaction between buyer and seller — not just the line items on the most recent commercial invoice.

Example of Transaction Value being Greater than the amount showing on the invoice

Consider this example of a manufacturer importing, a custom-made aluminum product:

The invoice accompanying the shipment shows a transaction value of $18,000 leading the customs broker- on behalf of the importer- to file an entry for customs with a value of $18,000. Customs accepts the tariff classification and country of origin, but stops the goods to question the value.

Upon further investigation, it is learned that the importer paid the manufacturer other amounts related to the importing goods. These payments were part of earlier transactions for such things as design, tooling, and prototype samples. Even though these were paid earlier and separately, these cost should have been included as part of the transaction value at import.

What gets added to declared value

Tooling charges, engineering and design fees, royalties and licence payments, and buyer-supplied materials or components ("assists" in customs terminology) all adjust the declared value when they are connected to the goods being imported. Payment on a separate invoice, in a separate transaction, in a separate currency, or even in a separate calendar year — none of that changes the rule. If the cost contributed to the production of the imported goods, and the buyer bore it, it forms part of the customs value. This is in addition to the transport and insurance (CIF) mentioned earlier.

The Takeaway: Transaction Value is "Price Paid or Payable for the importing goods"

If the transaction value is not clear, for example when importing free samples or inter-company merchandise, other methods of value are to considered in hierarchal order:

If Transaction value is not possible... consider other methods in the following order:

- Value of Identical goods

- Value of similar goods

- Deductive value

- Computed value

- Fall Back Method

2. The "No Sale" Valuation: The Hypothetical Standard

This is often referred to legally and financially as Fair Market Value (FMV). This type of valuation occurs when there is no actual transaction taking place. Instead, a valuator calculates what the business would be worth in a hypothetical open market.

These valuations are used for tax purposes, divorce settlements, estate planning, or 409A stock option pricing.

- Hypothetical Parties: It assumes a "hypothetical willing buyer" and a "hypothetical willing seller," neither of whom is under any compulsion to buy or sell.

- No Synergies: Crucially, this usually ignores strategic synergies. It assumes the business is being sold as a standalone entity, not as a strategic puzzle piece for a giant corporation.

- Regulatory Frameworks: It is bound by strict legal standards (like IRS Revenue Ruling 59-60) rather than negotiation tactics.

The Takeaway: "No Sale" Valuation is "Value." It is a theoretical baseline of worth, stripped of the specific motivations of a real-world deal.

Comparison: Why the Numbers Differ

The gap between these two figures can be significant. A "No Sale" valuation might value a company at $10 million (based on cash flow), while a Transaction Value could be $15 million (because a competitor wants to buy them to shut them down).

| Feature | Transaction Value (Price) | "No Sale" Valuation (FMV) |

|---|---|---|

| Context | An actual deal (M&A, Sale). | Compliance (Tax, Litigation, Reporting). |

| The Buyer | A specific person or company. | A hypothetical, generic buyer. |

| Synergies | Included (often drives price up). | Excluded (valued as standalone). |

| Emotion | High (negotiation, ego, timing). | None (objective analysis). |

| Outcome | Cash or stock changes hands. | A report is filed; no ownership changes. |

Summary

If you are selling your business, you are chasing Transaction Value—you want the highest price a strategic buyer will pay.

If you are gifting stock to your children or granting options to employees, you are using a "No Sale" Valuation—you want a defensible, objective number that satisfies the IRS or the courts.

The "First Sale Rule" (US Imports)

For high-volume importers to the USA, the First Sale Rule is a powerful financial tool. It allows the importer to declare the price the factory charged the middleman, rather than the price the middleman charged the importer, provided specific strict conditions are met.

Conditions for First Sale:

- The goods must be destined for export to the United States at the time of the first sale.

- There must be two bona fide sales (Factory to Middleman, Middleman to Importer).

- Paperwork must be flawless (purchase orders, invoices, proofs of payment).

Read our Deep Dive on First Sale Validation.

Wholesale vs. Retail Valuation

For e-commerce brands, the "Declared Value" depends on your logistics model. This choice can dramatically change your Landed Cost.

- Direct-to-Consumer (Cross Border): If you sell a shirt for $50 online and ship it to the customer, the declared value is $50 (Retail Price).

- Import for Warehouse (B2B): If you import 1,000 shirts to a warehouse to sell later, the declared value is the Manufacturing or Wholesale Price (e.g., $10).

This valuation gap is why many brands utilize a Non-Resident Importer (NRI) strategy to import in bulk at lower values before selling to the end consumer.