With increased online shipping to Canada, more questions are being raised about the import clearance costs in Canada. Especially from the US, shippers are often surprised to know that most parcel shipments to Canada are subject to duty and import fees.

Below is information to help shippers understand the Canadian Customs (CBSA) and carrier clearance costs when shipping internationally to Canada.

Understanding import costs for online parcel import to Canada from the USA, Europe and Asia includes duty, taxes and carrier fees.

All items shipped to Canada - including from the USA - may be subject to duty and taxes. Canadian customs/ CBSA calculates duty rates according to the type of goods you are importing and the country from which they came or were made. Additional taxes, such as excise duty or excise tax may apply to specific items such as alcohol and tobacco products.

This blog helps explain the import fees for online orders and consignments imported to Canada.

The that factors affect duty and import fees for goods imported to Canada include:

- From where the goods are shipped: See chart below

- Method of shipping (Postal, Ground, Air Courier)

- Country of Origin (if eligible for preferential duty free import)

- Value of the consignment (click on link below to read more about valuation)

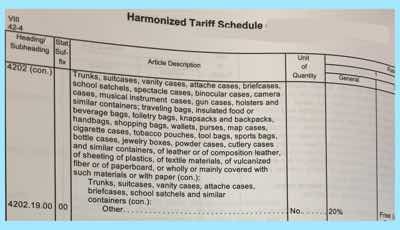

- Harmonized code / HS code (read more about HS Codes)

Contact our team for an initial consultation.

How to avoid customs fees Canada

Customs fees are unavoidable in most cases. However, you can reduce import fees by choosing air versus ground shipping. Also, many report that import fees via the post are less than via a commercial carrier. Even if they are technically subject to the same duty and taxes.

You may also save fees by applying the correct country of origin, declared value and HS code.

What is Canada Import Tax?

What is a Canadian Surtax?

Shipped From ≠ Country of Origin

Shippers are often confuse the concepts of country of origin as being from where the goods are shipped. The country of origin refers to where the goods were made and shipped from is .... well.. where the goods were shipped from.

Read More: Country from where goods were shipped versus country of origin import to Canada

- Consignments shipped from Mexico and Canada enjoy a higher duty free threshold (see chart below)

- If the goods are made in a country that has a free trade agreement with Canada (USMCA, CPTPP, CETA, CKFTA etc) they may benefit from preferential duty free import regardless of value.

Benefiting from Canada's many Free Trade Agreements

Goods made in the USA, Europe and other countries with a Canadian free trade agreement are not automatically granted duty free status. To qualify for duty free status under NAFTA/ USMCA, CETA or other free trade agreement, the goods must meet certain criteria (most importantly related to having a qualifying certificate of origins).

READ MORE: VERIFY IF A CERTIFICATE OF ORIGIN IS NEEDED

See note below on NAFTA/ USMCA, CETA and CPTPP country of origin requirements for duty free entry to Canada.

Canada’s Most Favoured Nation (MFN) tariff rates are generally applicable to imports from most countries. Preferential duty free import is available for goods that meet the rules of origin under the terms of Canadas many trade agreements.

Complete list of countries that may benefit from duty free import to Canada.

Postal Solution Shipping To Canada

Jet Worldwide provides parcel import and last mile delivery solutions from France, UK, Spain and all the EU to Canada. Parcel clearance solutions include LVS - Low Value Shipment solutions, foreign importer of record, and single importer of record.

Basic rules for importing parcels to Canada

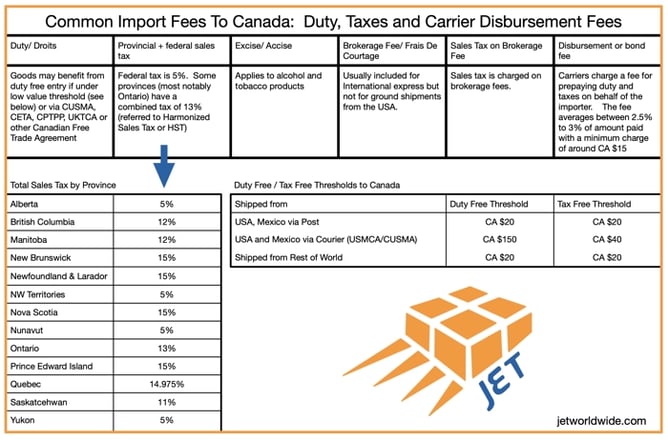

Most consignments imported to Canada valued over $20 CAD (or $40 CAD if shipped from USA or Mexico) are subject to duty and/or taxes.

See chart below: Duty free low value threshold to Canada.

Duty Free Shipping to Canada from the USA:

The low value duty threshold for consignments shipped from the USA ( de minimis threshold) can be as high as to $150 CAD (around $110 USD). The duty free threshold varies according to from where the goods are shipped and method of shipping. See chart below.

Local sales taxes will still apply (but often times, businesses can claim this charge back). This higher duty free threshold helps businesses and e-commerce merchants in the United States ship to Canadian customers.

Shipments valued under $40 CAD - and shipped via courier (versus USPS) can be imported to Canada free of duty and taxes. For goods shipped via USPS, the low value duty free threshold is $20 CAD.

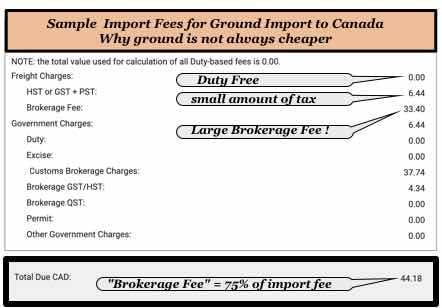

Shipping Ground to Canada from the USA

Ground shipping is often the most cost effective method for shipping to Canada but the cost advantage can be offset by longer transit times and customs entry preparation fees.

The entry preparation fees below are representative costs only as they are subject to change and can be negotiated with the carriers.

Useful PDF: FedEX and UPS import fees to Canada

Important to consider "entry preparation cost when sending ground to Canada (versus express)

Canada Express LVS Clearance

Canada’s LVS system allows for streamlined clearance processes but does not give preferential treatment with respect to import duty and taxes. Goods shipped via courier to Canada valued under $3,300 CAD can be cleared using the LVS system.

Main components of imports fees to Canada explained below:

- Duty: Depends upon value, commodity code, country of origin and from where goods are shipped.

- Taxes: Federal and provincial sales tax applies to customs

- Clearance entry preparation fee: Primarily applied to ground shipments. This fee is most often included for air express shipments to Canada

- Disbursement fee: Carriers charge a fee when duty and taxes are paid on behalf of the receiver prior to delivery.

Delivery to and from Canada

Jet Worldwide: A trusted brand offering international shipping for over 40 years!

Jet Worldwide provides Canadian logistics support regarding international and Canadian movement of goods. This can include things like transportation, storage facilities, and supply chain management. Our logistics support augments your team by not being beholden to a specific carrier or process.

Duty Rates for Online Orders to Canada

Similar to all major economies that adhere to WTO rules, Canada bases their duty primarily on the declared value, commodity / H.S. Code, and country of origin. The duty rate for common imports such as clothing, can be as high as 20%.

Get support for your Amazon Shipments to Canada with Jet's team

Goods made in the USA (as well as from other countries that share free trade agreement with Canada) are not automatically granted duty free status to Canada. Items that qualify for duty free status under USMCA, CETA, CPTPP, CKFTA or other free trade agreement must include qualifying certificate (or certification) of origin.

Customs Preparation Fee for Consignments to Canada

A customs entry must be made for every parcel imported to Canada. Most express and postal shipments include the “Customs Entry Preparation Fee.”

For shipments sent via FedEx and UPS Ground to Canada, the Customs Preparation fee is not included. For high volume shippers, this fee can be negotiated but most ground shippers to Canada pay a customs entry preparation that is based on the “value for duty” of the shipment. The entry preparation fee can be as low as $7 and progressively gets more expensive roughly averaging around 20% of the value of the shipment.

For example, a shipment valued at $300 CAD sent via FedEx or UPS ground to Canada could be charged a clearance entry preparation fee of around $45 CAD.

Registration in CARM

All commercial importers must register in CBSA's CARM system. Doing so requires importers to assign a customs broker and submit a surety bond (or deposit) to guarantee payment of duty and taxes. How to register for CARM.

What is the difference between CARM and CERS?

Carrier Disbursement Fee charged in Canada

Even when entry preparation fee is included, carriers charge a fee to cover their cost of advancing the duty cost on behalf of the receiver. The costs are calculated as a percentage of the duty and taxes paid (usually around 2.5% of the value) with a minimum fee that averages around $15 CAD.

Processing Fee for consignments imported to Canada

In addition to the disbursement fee, carriers charge a fee for having to get payment from importers who do not have an account with the carrier who paid the import fees on their behalf . The “processing fee” is around $10-$20 and is applied regardless of whether the shipment was sent ground or air.

- Shipments above low value thresholds are subject to duty/ taxes

- For most air express services "Entry preparation" included

- Import charges include Duty, taxes, plus a $16 (minimum . *see following two points) processing ($11) + transaction fee ($5)

- Processing fee: $11.00 or 2.5% of the Duties and Taxes (which ever is higher)

- Transaction Fee: $5.00

- Shipments above $3,300 or otherwise requiring additional processes or approvals (such as alcohol) are subject to additional fees

Many countries have a general consumption tax which is assessed on the value added to goods and services. In some countries such as Canada, Singapore, Australia, and New Zealand, this tax is known as the goods and services tax or GST.

The Canadian sales taxes are the Provincial Sales Tax (PST), the Quebec Sales Tax (QST), the Goods and Services Tax (GST), and the Harmonized Sales Tax (HST) which is a combination of the PST and the GST in some provinces.

Any item mailed to Canada may be subject to the Goods and Services Tax (GST) and/or duty. Unless specifically exempted, you must pay the 5% GST on items you import into Canada by mail. The CBSA calculates any duties owing based on the value of the goods in Canadian funds. The duty rates vary according to the type of goods you are importing and the country from which they came or were made in. Depending on the goods or their value, some other taxes may apply, such as excise duty or excise tax on luxury items.You do not have to pay the GST on the following goods that are imported into Canada by mail:

- goods worth CAN$40 or less; and

- gifts from family members or friends who live abroad when the worth is CAN$60 or less.

The Government of Canada has entered into agreements with certain provinces to collect the HST at a rate of 13 percent. If you live in a participating province, you will have to pay the HST instead of the GST.

It depends on the contents, value and origin of the shipment. You may be charged the following:

- Duties and taxes

- FedEx Reimbursement on Delivery Fee or Advancement Fee

- Ancillary charges, if applicable. For more details, please visit fedex.ca/ancillary.

Low-Value Entry Exceptions for shipments imported to Canada via FedEx, UPS or DHL

Low-value shipments are valued under CAD$3,300. Under CBSA regulations, low-value shipments can be “provisionally released” for delivery pending payment of duty/ taxes and - if required - a formal entry.

Canadian customs / CBSA assess duties and taxes based on criteria that includes:

- Product value

- Trade agreements

- Country of manufacture

- Description and end use of the product

- The product's Harmonized System (HS) code

Import Fees for Gifts Shipped to Canada

For eligible gifts imported into Canada valued less than CAD$60 or less per shipment can be imported duty/ tax free. Shipments of gifts over CAD$60 is subject to duties and taxes on the amount over $60 (for example, a qualifying gift of $200 would be subject to duty/ taxes based on a value of $200-$60 or $140).

Canada Post: Less likely to collect import duty and taxes

Due to the sheer volume and less developed electronic processes, many shipments sent via Canada Post are delivered without duty or taxes being charged to the importer. While this is a windfall for the buyer, the inconsistency creates issues when they are charged. And, duty free thresholds are more restrictive under CUSMA versus shipping via express carrier/ courier.

Different duty assessment for goods shipped via USPS versus Courier (see below regarding new USMCA/CUSMA duty free thresholds).

For a shipments shipped via USPS for import via Canada Post, duty is assessed differently than for parcels shipped via parcel carriers/ courier:

- CA $20 (around US$14.75) and under: duty and tax free

- Above CA $20duties and taxes apply

Shippers who receive goods without charge via Canada Post are often shocked when they are forced to pay duty and taxes on goods. The inconsistency creates mistrust and dissatisfied buyers who ended up paying much more than what they expected. Even if the duty and taxes are properly calculated as required by law, online forums are ripe with comments wondering if the fees are actually legitimate.

Duty Free Canada Import via NAFTA/ USMCA, CETA, CPTPP and others

A certificate of origin is the exporter's certification that the good being exported meets a free trade agreement's rules of origin and therefore qualifies for preferential tariff treatment afforded under the relevant agreement. Modern trade agreements allow for a statement or "certification of origin" that can be included on the shipping paperwork (most commonly the invoice for customs) rather than a separate certificate.

Information concerning the rules of origin for each free trade agreement can be obtained online via CBSA websites.

USMCA / New NAFTA duty free clearance for online orders to Canada

Online orders containing US or Mexico origin goods can qualify for for duty free entry entry to Canada.

The CUSMA facilitates the movement, release and clearance of good via a simplified framework and standardized customs procedures. Trade facilitations includes fewer clearance formalities for “express shipments” valued under CA$3,000 (to Canada) and US$2,500 (to the USA and Canada).

Check out theCanadian Border Services Agency (CBSA) page that describes the new requirements for more information and an example of a valid CUSMA certification of origin.

CUSMA/USMCA Shipping to Canada from the USA

The key provisions of CUSMA USMCA (i.e. new NAFTA) include:

- Duty free and tax free entry for most US origin parcels shipped courier valued under CA$40

- Duty free entry for most parcels shipped courier from the US valued under CA$150

- Simplified "Certification of Origin" for shipments sent via courier valued under CA$3,300

The duty free threshold to Canada changes based on where consignment is shipped from and how it is shipped.

For low value shipments (under CAD $3,300 to Canada) a certifying statement added to the commercial invoice or any shipping document

“I hereby certify that the goods covered by this shipment qualifies as an originating good for the purposes of preferential tariff treatment under USMCA/T-MEC/CUSMA.”

This statement can be included on the commercial invoice as long as shipment values fall below these thresholds.

Duty-free import for parcels sent from Europe, Asia and all countries with a Canadian Free Trade Agreement

Canada has free trade agreements will most of the world's major economies.

- UK: UKTCA

- France, Germany, Spain, and European Union Countries: CETA

- South Korea: CKFTA

- Japan, Singapore, Australia, New Zealand and Asia Pacific: CPTPP

Consignments that qualify as originating (via the many Canadian free trade agreements) valued less than CAD 3 300 do not require a certification of origin to claim preferential tariff treatment.

Parcels containing products under CAD 3 300 can be considered for duty-free status if the following conditions are met:

- A signed statement completed by the importer, exporter or producer certifying that the goods originated from the country with a corresponding free trade agreement is included. This statement is required on the commercial invoice and we recommend adding an additional stand alone statement/ supporting document.

- The goods meet the origin rules under the terms of the agreement. For example, marks to indicate that the goods are not a product of the origin country will disqualify the goods and have issues related to mis-declarations.

US online orders to not automatically qualify for NAFTA USMCA duty free

Just because the origin of the goods being shipped are from the USA or Mexico does not mean the goods qualify for duty free entry.

As mentioned above: To qualify for preferential duty free import to Canada, the goods must be actually made in Canada or Mexico: Shipping from ≠ Country of Origin.

Read more: Difference between from where goods are shipped and country of origin of the goods.

Qualifying for duty free CUSMA status without a certificate of origin

A CUSMA Certification of Origin can be included on shipping documents (including the invoice for customs) to request preferential duty free entry to Canada. See above.

Other things to consider when shipping to Canada include:

- Importer of record: The importer of record includes having to obtain an importer number. If to direct to consumers, the consumer can be the importer of record

- Provincial licenses may be required even if selling direct to consumers

- Federal and provincial sales taxes (read about Canadian import fees)

- Health Canada approvals for related products

- Safe Foods for Canadians Act certifications for some food items

- Tariff classification for all imports (read more about HS Codes)

- Country of Origin must be declared for all imports.

- Valuation is an important part of the declaration to the CBSA (read more about valuation).

- Labeling for goods to Canada may require both French and English.

- Certification of origin if duty free import requested under a free trade agreement

Getting a quote for shipping to and from North America

We are happy to help with your shipping to Canada. Please provide some more information about the type of goods that will be shipped, and whether they are being sent via air or sea freight? Additionally, it would be helpful to know the volume of goods and items being shipped. What restrictions or regulations are you aware of that should be taken into account?

Choosing the Best International Shipping option to Canada

- Local post options are generally best for individuals shipping to Canada

- Air freight: This is the fastest option with economy air options

- Ocean: Best for large commercial orders

- Trucking: A good options for shipping pallets, less than truck load (LTL) and full truck loads between Mexico, USA and Canada,

- FedEX , DHL, UPS: Well known brands with air options (and international ground between Canada and USA). Shippers can access the carriers directly for via one of their partners.