European countries are implementing rules that make importing e-commerce more transparent and consistent across borders. For all orders, it is now mandated that VAT be collected at the point of checkout. Goods can then be cleared using a streamlined "green channel" for faster processing and, most importantly for e-commerce sellers, zero consignee fees.

Value-added tax (VAT) is a consumption tax added to the price of goods and services in the European Union (EU). In the context of e-commerce imports, VAT is applied to goods purchased from non-EU sellers and imported into the EU.

Quick Answer: How Do You Ship E-commerce to Europe from Canada in 2026?

Register for the Import One-Stop Shop (IOSS) so you can charge VAT at checkout on parcels under 150 euros, deliver through the green channel with no surprise fees, and report through a single EU registration. From 1 July 2026, the duty-free threshold ends and a 3 euro customs duty applies per line item on parcels up to 150 euros. The IOSS holder becomes the legally responsible declarant, consolidated clearance for low-value B2C parcels is being phased out, and from 1 November 2026 a new handling fee and a mandatory product identifier per line item will apply.

Key Takeaways for 2026:

- The EU Customs Reform reshapes how B2C parcels are treated, rolled out in stages through 2028.

- Stage one (July 1, 2026): the customs duty-free threshold ends and a 3 euro duty applies per line item.

- Consolidated clearance for low-value B2C parcels into the EU will be very limited.

- EU customs increasingly expect an established EU presence to act as Importer of Record.

- From November 1, 2026: a new EU handling fee and a mandatory line-item Product Identifier for all B2C imports.

- Across every stage, complete and accurate electronic invoice data is the key to smooth clearance.

Jet Worldwide offers a comprehensive suite of shipping services designed to help e-commerce businesses efficiently and reliably deliver their goods to customers across various European countries.

The 2026 EU Customs Reform: A Timeline

The EU Customs Reform (EUCR) is being implemented in stages. These are the dates that matter for anyone shipping e-commerce into the EU27:

The customs duty-free threshold is eliminated. A 3 euro customs duty applies per line item on parcels up to 150 euros. Consolidated clearance for low-value B2C parcels becomes very limited, and stricter clearance-location rules apply.

A new EU customs handling fee is introduced (a regulatory fee in addition to duty), and a mandatory Product Identifier is required at line-item level for all B2C imports.

The comprehensive customs reform and the EU Customs Data Hub are expected to take effect, replacing the temporary measures with full per-item tariff calculation.

Importing Low-Value Shipments to Europe: 2026 Update

The end of the 150 euro threshold: what it means for you

One of the most significant changes in recent EU customs policy is the practical elimination of the "low-value" duty-free threshold. Historically, many shippers relied on the 150 euro limit to avoid the cost and complexity of duty structures. From July 2026, Europe imposes a 3 euro customs duty per line item on these shipments.

The 3 euro duty is multiplied by each distinct item category, mainly identified by the 6-digit Harmonized System code and the country of origin, contained within the parcel.

Example Calculation:

- The order: 4 silk blouses plus 2 wool blouses plus 1 pair of leather shoes.

- The assessment: Silk blouses, wool blouses, and leather shoes each fall under a different tariff sub-heading, so there are three distinct categories in the box.

- The cost: 3 categories multiplied by 3 euros equals 9 euros total customs duty.

Tip: group items that share the same tariff classification on a single line so the 3 euro charge is not applied more times than necessary.

These temporary fees are intended as a bridge to the comprehensive 2028 customs reforms. Note that the precise way the 3 euro duty will be billed to the private consumer is still being defined; once the legislation and carrier processes are finalized, the practical impact will become clearer.

Industry experts warn that these fixed costs risk hollowing out the Import One-Stop Shop (IOSS) scheme by making the "simplified" route more expensive and complex than standard customs procedures. If charges cannot be collected digitally, the burden may revert to couriers, reintroducing "cash-on-delivery" delays and eroding the seamless checkout experience IOSS initially promised.

What Counts as a B2C Shipment Under the Reform

The reform puts B2C shipments at its core, driven by the massive growth of low-value parcels entering the EU27. A shipment is considered B2C when it meets all of the following criteria:

- It is shipped from a non-EU27 country into an EU27 member state.

- The seller is a business.

- The final consignee is a private consumer.

- Transport is arranged by the seller.

- The goods are shipped directly from the non-EU seller to the EU consumer and are pre-labelled.

- The goods are intended for private consumption.

Low-value shipments of 150 euros or less are in scope for both B2C and B2B. For B2B parcels up to 150 euros, the reduced H7 dataset is no longer allowed; they must be cleared through a full formal H1 declaration and are subject to actual or, where applicable, preferential duty rates.

Understanding IOSS and Simplified VAT Reporting

The VAT rate applied to imported goods depends on both the country of origin and the destination country. Generally, the VAT rate applied to imported goods matches the domestic VAT rate for similar items.

Import One-Stop Shop (IOSS) is an EU-wide system that streamlines the process of collecting and remitting VAT on e-commerce imports. Non-EU sellers registered under IOSS can collect and remit VAT on their sales directly to EU customers.

Because the VAT is collected at the point of sale, the seller simply remits the total to the EU. Customers do not need to pay surprise VAT fees upon delivery, allowing sellers to offer a highly seamless shopping experience.

Green Channel Import and IOSS Quarterly Reporting

IOSS functions as a quarterly filing submitted to a tax authority in the same format as standard VAT OSS. It allows Canadian and US sellers to register in one single EU country while legally selling across the entire EU bloc. This means one set of reporting and one consolidated payment.

Read more: Shipping Shopify orders to Europe from Canada

Why Clearance Location Now Matters: IOSS versus Non-IOSS

One of the most practical changes in the reform is where a parcel may be cleared. This is a strong reason to use IOSS:

- Consolidated clearance for low-value B2C parcels (150 euros or less) is no longer possible under current understanding. High-value B2C parcels above 150 euros and B2B parcels are not affected.

- Non-IOSS B2C parcels of 150 euros or less must be cleared in the destination member state. It is no longer allowed to clear them at the first point of entry if the goods are destined for a different member state.

- Carriers now require individual information for each parcel, such as value per parcel and seller and buyer details, submitted in the electronic shipment data.

For example, a non-IOSS B2C order worth 60 euros sold to a customer in Italy can no longer be cleared at a central entry point in another country; it must be cleared in Italy. Using IOSS preserves clearance flexibility and keeps the consignee experience clean, which is why it remains the preferred route for direct-to-consumer sellers.

IOSS Holders Are Now the Declarant

Under the reform, the IOSS holder becomes the declarant and is legally responsible for the customs import clearance:

- For IOSS shipments, the carrier completes the import clearance on behalf of the IOSS holder, not the final consignee.

- The IOSS holder therefore becomes legally responsible for the clearance.

- The carrier requires additional information from the IOSS holder, including name and address, confirmation of whether the holder is EU-established, and, where available, the EORI number and VAT ID.

Please note: if a platform or marketplace is registered for IOSS, IOSS use is mandatory in the import clearance, and selection per individual shipment is not possible.

VAT Rules for E-commerce Imports from Canada

Note: Registration for IOSS is not mandatory for e-commerce sellers shipping from North America to a specific country. A seller shipping exclusively to France from Quebec, for example, can choose to pay the VAT at the time of import and bypass IOSS registration entirely.

The IOSS Process and Portal

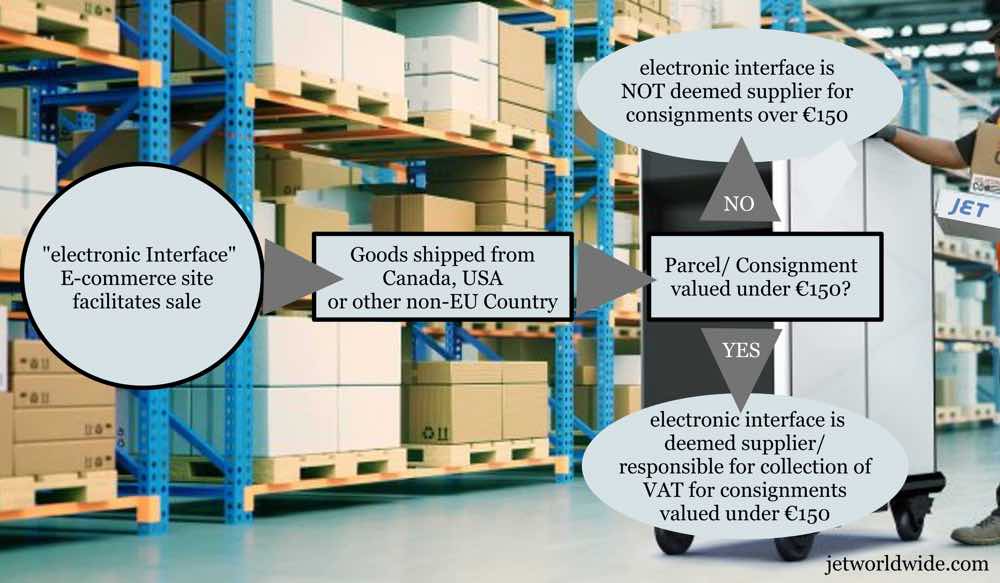

For e-commerce shipments valued under 150 euros, IOSS allows sellers and online marketplaces to charge VAT at the point of sale and remit it directly to the authorities.

- If IOSS is not used, the importing carrier will charge the VAT to the e-commerce customer upon delivery (which usually includes an added administrative or pre-payment fee).

- Canadian e-commerce businesses and marketplaces only need to register for a VAT account in a single EU country, rather than registering in every country they ship to.

VAT Collection by Marketplaces and Sellers

Online marketplaces or direct-to-consumer (DTC) sellers are responsible for collecting VAT for orders up to 150 euros. Merchants using multiple marketplaces must keep accurate sales records corresponding to the IOSS number or customs declarant used for each transaction.

Coverage Across All EU Countries

IOSS applies to online sales spanning all EU countries, including Austria, Belgium, France, Germany, Italy, Spain, and Sweden, among others. EU VAT rules for Northern Ireland are established separately under the EU-UK Joint Protocol.

For official details on IOSS and the EU VAT rules, visit the Publications Office of the European Union.

Facilitating Registration and Integrated Shipping

Partnering with a logistics expert simplifies the entire process. Here is how it works:

- Get an approved account with Jet Worldwide.

- Register for IOSS.

- Ship directly to consumers in Europe.

- Enjoy lower costs, full tracking, and no surprise import fees charged to your consignee.

Becoming EU-Established: The Importer of Record

Under the reform, EU customs authorities place increasing emphasis on having an established presence within the EU that can act as Importer of Record (IOR). The Importer of Record is the entity responsible for ensuring goods are imported in accordance with the laws and regulations of the importing country. The benefits of an EU-established Importer of Record include:

- Clear responsibility and a clear point of contact for EU customs authorities.

- Centralized control and visibility of EU customs activities.

- Access to future reform simplifications.

- More predictable customs clearance and less risk of delays or disruptions.

From July 1, 2026, it is important to know whether you are an EU-established entity that can act as Importer of Record, or whether you use an EU-based customs representative. Be ready to provide your name and address, EORI number, VAT ID, and confirmation of whether an EU-based company can act as your Importer of Record. B2C goods should show the retail value on the commercial invoice, and it is important to understand how the Anti-Abuse Clause (Article 243(5) of the UCC Implementing Act) applies to your shipments. External advisors, including Jet Worldwide, can help you become EU-established in a compliant way through VAT and EORI registration.

EORI Numbers for Business Importers

While IOSS is designed for e-commerce orders sent to individuals (B2C), shipping from Canada to Europe for business purposes (B2B) requires verifying the EORI number of the consignee.

An Economic Operators Registration and Identification number (EORI number) is an identification number for businesses that import or export goods into or out of Europe. It is a mandatory part of the data set required for customs entries in all EU countries. The EORI number consists of two parts:

- The country code of the issuing member state.

- A code or number that is completely unique within that member state.

Coming November 2026: Handling Fee and Product Identifiers

The EU Customs Handling Fee

Targeted for November 1, 2026, a new EU customs handling fee is expected to apply to B2C shipments from the rest of the world into the EU27, with no value threshold mentioned in the proposal at this stage. It is a fixed regulatory fee charged per line item, in addition to any applicable customs duty. The exact amount, exemptions, and treatment of returns are not yet confirmed; industry estimates point to roughly 2 euros per item, but the official figure is still pending. Note that national handling fees already introduced in countries such as France and Romania are independent of the EU handling fee, and it is not yet known whether those national fees will be removed once the EU fee takes effect.

The Mandatory Product Identifier

Also from November 1, 2026, all B2C goods imported into the EU27 will require a new mandatory line-item field to complete customs clearance: the Product Identifier. A Product Identifier is a unique code that clearly identifies a specific product so it can be tracked through the supply chain. There are two types:

- Merchant Product Identifier: a code assigned by the online seller, marketplace, or platform.

- Manufacturer Product Identifier: either non-standardized (created internally by the manufacturer or brand, such as an internal SKU or article number) or standardized (based on internationally recognized standards such as GTIN, MPN, or EAN).

Sellers should begin mapping these identifiers to their catalogue now, since clean, standardized product data will be essential for smooth clearance once the requirement applies.

Returns and Duty Refunds Under the New Rules

Customs duty refunds for B2C returns of 150 euros or less are no longer available, whether the goods were cleared under a formal H1 or reduced H7 declaration. The current VAT refund rules for B2C returns are unchanged. Customs duty refunds still apply for defective goods, B2B returns, and non-distance-sales goods.

Frequently Asked Questions

Do I need IOSS to ship e-commerce to Europe?

IOSS is not mandatory, but it is strongly recommended for parcels under 150 euros. Without it, the carrier charges VAT to the consumer on delivery, usually with an added fee, and a non-IOSS B2C parcel must be cleared in the destination member state. IOSS lets you collect VAT at checkout, deliver through the green channel, and report through a single EU registration.

How is the 2026 EU 3 euro customs duty charged?

From 1 July 2026, parcels up to 150 euros lose the duty exemption and a 3 euro duty applies per line item, identified mainly by the 6-digit HS code and country of origin. Each distinct tariff category attracts its own charge; multiple identical items on one line attract a single charge.

What counts as a B2C shipment under the reform?

It must meet all of these: shipped from a non-EU country into an EU member state, the seller is a business, the final consignee is a private consumer, transport is arranged by the seller, the goods ship directly to the consumer and pre-labelled, and they are intended for private consumption.

Can I still use consolidated clearance for low-value parcels?

Under current understanding, consolidated clearance is no longer possible for low-value B2C parcels of 150 euros or less. High-value B2C parcels above 150 euros and B2B parcels are not affected. Carriers now need individual data for each parcel.

Who is legally responsible for customs clearance under IOSS?

The IOSS holder becomes the declarant and is legally responsible. The carrier clears on behalf of the IOSS holder, not the consignee, and will request the holder name and address, EU-establishment status, EORI, and VAT ID. If a marketplace is registered for IOSS, IOSS use is mandatory and cannot be selected per shipment.

What changes on November 1, 2026?

A new EU customs handling fee per line item (a regulatory fee in addition to duty, amount not yet confirmed), and a mandatory Product Identifier per line item for all B2C imports, which can be a merchant identifier or a manufacturer identifier such as an internal SKU or a standardized GTIN, MPN, or EAN.

Can I get a customs duty refund on a B2C return?

No. Duty refunds are no longer available for B2C returns of 150 euros or less, under either H1 or H7 clearance. VAT refund rules for B2C returns are unchanged. Duty refunds still apply for defective goods, B2B returns, and non-distance-sales goods.

Do I need an EORI number to ship to Europe?

For B2B shipments you must verify the consignee EORI number. An EORI number identifies businesses importing or exporting goods into or out of Europe and is a mandatory part of the customs data set in all EU countries.

Shipping to Europe: A Major Opportunity for E-commerce

The import landscape into Europe presents a massive growth opportunity. European consumers are accustomed to paying VAT, and charging it transparently at checkout actually builds brand credibility. Knowing your goods will be delivered without hidden import fees is a major competitive advantage.

Resource: Useful information regarding import duty calculations

Shipping Online E-Commerce Orders to Europe

Jet Worldwide provides global logistics solutions tailored for Canadian and US businesses. Our logistics support augments your team, ensuring you are never restricted by a single carrier or rigid process.

- Parcel shipping solutions from North America to Europe and the UK for online orders.

- Delivery VAT and Duty paid import solutions for B2C e-commerce consignments.

- World-class logistics support from industry experts.

Timothy Byrnes — Jet Worldwide

Timothy has led Jet Worldwide, a Montreal-based international logistics and customs brokerage firm, since 1988, specializing in Canada-Europe e-commerce, IOSS, and EU customs compliance. More about our team.

Disclaimer: The information in Jet Worldwide online content, including this post, is for general information only and provided "as is"; no representations are made that the content is error-free.