Quick answer: From July 1, 2026, a new customs duty of 3 euros per distinct item applies to all e-commerce parcels entering the European Union where the goods are valued at 150 euros or less. This replaces the previous duty exemption. Canadian online sellers shipping to EU consumers must understand two customs entry pathways: H7 (simplified e-commerce declaration for low-value B2C shipments) and H1 (traditional full customs entry for higher-value or commercial shipments). Registering for IOSS (Import One-Stop Shop) lets Canadian sellers collect VAT at checkout and use the streamlined H7 process.

New Rule Effective July 1, 2026

The EU has eliminated the customs duty exemption for e-commerce parcels valued at 150 euros or less. A flat 3 euro duty per distinct item category in each parcel now applies across all 27 EU member states. An additional 2 euro handling fee per consignment applies from November 2026. VAT (ranging from 17% to 27% depending on the member state) continues to apply on top of the duty.

The New 3 Euro Per Item Customs Duty (Effective July 1, 2026)

From July 1, 2026, a new customs duty of 3 euros for each distinct item category in a parcel applies to goods purchased online from non-EU countries, including Canada. This change applies uniformly across all 27 EU member states.

How the 3 euro duty is calculated

The duty is assessed per distinct item category (including tariff sub-category) in the shipment, not per parcel. For example:

Example 1: A package from Canada contains a pen, a notebook, and a key ring. Each distinct item has a 3 euro duty charge: 3 items x 3 euros = 9 euros customs duty, plus VAT.

Example 2: A package contains two identical pens. These are considered one item category: 1 category x 3 euros = 3 euros customs duty, plus VAT.

Example 3: A Canadian Shopify seller ships one silk scarf and four wool scarves. Silk and wool fall under different tariff sub-headings, creating two distinct categories: 2 categories x 3 euros = 6 euros customs duty, plus VAT.

Important not: The 3 EUR duty applies to each unique HS code, per declaration line. Multiple items with the same tariff classification should be on a single line on the invoice to avoid the 3 Euro duty being applied unnecessarily.

From November 2026, an additional 2 euro handling fee per consignment is expected.

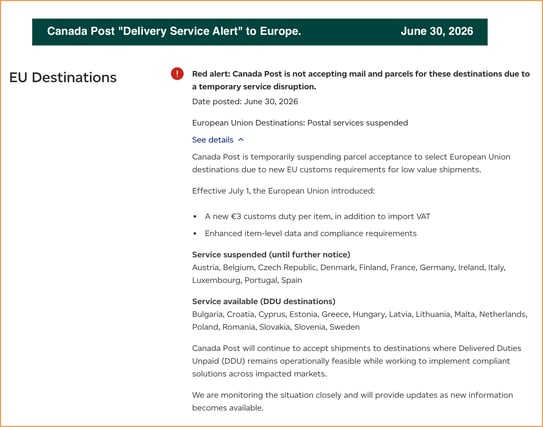

Options now that Canada Post has suspended service to Europe?

Canada Post announced a suspension of service to France, Germany, Spain, Portugal, Ireland nd other major European countries on June 30, 2026.

For small shippers, the best option of using commercial carriers (or their partners) but the costs are much more than the small packet service offered via the post

Large shippers should look to build direct shipping processes to Europe: Consolidate, ship via air freight, dedicated clearance process, distribute across Europe. Contact our team for details.

H7 vs H1: Two Customs Entry Pathways into the EU

When goods arrive at an EU border, they must be declared to customs through a formal entry. The EU customs system offers two distinct declaration types for imports, and understanding the difference is essential for Canadian e-commerce sellers:

H7 — Simplified Low-Value E-Commerce Declaration

The H7 dataset is a streamlined customs declaration designed specifically for B2C (business-to-consumer) e-commerce shipments valued at 150 euros or less. It was introduced as part of the EU's July 2021 e-commerce VAT reform alongside the IOSS system.

Key characteristics of H7:

- Fewer data elements: H7 requires approximately 15 data fields, compared to 50 or more for a standard H1 declaration. This makes filing faster and less expensive.

- No full tariff classification required: Goods do not need a full 8 or 10 digit HS/CN code. A simplified commodity description is sufficient in most cases.

- IOSS integration: When the seller is registered for IOSS, the IOSS VAT identification number is included in the H7 declaration. This tells EU customs that VAT has already been collected at checkout, allowing the parcel to clear without the recipient paying VAT on delivery.

- Used by postal operators and express carriers: Postal services and courier companies (FedEx, UPS, DHL, national postal operators) file H7 declarations in bulk for the low-value parcels they carry.

- Value ceiling: Strictly for qualifying goods with a value less than 150 euros. Above this threshold, a H1 declaration is necessary.

- Goods excluded: Goods requiring specialized treatment, including alcohol, tobacco, some cosmetics and supplements do not qualify for H7 import processes.

July 2026 change: Before July 1, 2026, H7 shipments cleared with zero customs duty (only VAT applied). From July 1, 2026, H7 shipments are subject to the new 3 euro per item/per line duty in addition to VAT. The H7 simplified declaration process itself remains available — only the duty treatment changes.

H1 — Traditional Full Customs Declaration

The H1 dataset is the standard, full-format customs declaration used for all imports that do not qualify for H7 simplified treatment. This includes:

- All shipments valued above 150 euros

- All B2B (business-to-business) commercial shipments regardless of value

- Shipments containing excise goods (alcohol, tobacco, perfume, supplements)

- Pallet and freight shipments, FCL and LCL ocean consignments

Key characteristics of H1:

- Full data requirement: 50 or more data fields including complete 8 or 10 digit commodity code (Combined Nomenclature), country of origin, customs valuation, EORI number of the importer, transport document references, and detailed goods description.

- Traditional duty calculation: Duty is calculated based on the applicable tariff rate for the specific HS code. In many cases, this may actually be an advantage and involve lower duty. For Canadian-origin goods, CETA preferential duty rates (often 0%) can be claimed if a valid origin declaration is provided.

- EORI required: The EU importing business must have a valid EORI number (Economic Operators Registration and Identification).

- Higher compliance cost: A customs broker typically prepares the H1 entry, adding brokerage fees of 15 to 50 euros per declaration depending on the complexity. Couriers usually charge less than independent brokers. Regular importers most often find the benefit from having their own dedicated broker worth the additional cost.

H7 vs H1 comparison at a glance

| Feature | H7 (Simplified) | H1 (Traditional) |

|---|---|---|

| Value limit | 150 euros or less | No limit |

| Typical use | B2C e-commerce parcels | B2B, high-value, commercial |

| Data fields | ~15 (simplified) | 50+ (full dataset) |

| HS code required | Simplified description | Full 8-10 digit CN code |

| Customs duty (from July 2026) | Flat 3 euros per item category | Full tariff rate by HS code (CETA 0% if qualified) |

| VAT collection | Via IOSS at checkout or on delivery | Collected at import by customs broker |

| EORI required | Not for the buyer | Yes (importer of record) |

| CETA preference available | No (flat rate applies) | Yes (0% duty with origin declaration) |

| Brokerage cost | Minimal (bulk filed by carrier) | 15 to 50 euros per entry |

Send direct to Europe from Canada and get H1 clearance

Jet Worldwide offers Canadian e-commerce sellers access to H1 clearance for their European orders. This program offers a significant discount versus couriers and a for superior service to postal options. Contact our team for details.

IOSS (Import One-Stop Shop) for Canadian Sellers

The Import One-Stop Shop (IOSS) is an EU VAT registration mechanism that allows non-EU sellers (including Canadian e-commerce businesses) to collect VAT at checkout and remit it to a single EU member state, which then distributes it to the destination country.

Why IOSS matters for Canadian Shopify and e-commerce sellers

-

Better customer experience: When you collect VAT at checkout via IOSS, your EU customer pays the final all-in price and receives the parcel without any surprise charges on delivery.

-

Faster customs clearance: Parcels with a valid IOSS number clear customs more quickly.

-

H7 simplified declaration: IOSS shipments are declared through the H7 simplified process, reducing data requirements and compliance costs per parcel.

-

Applies only to B2C under 150 euros: IOSS covers distance sales of goods with an intrinsic value of 150 euros or less shipped from outside the EU to consumers. B2B sales and higher-value shipments require the H1 process.

Will IOSS be available for shipments over €150?

They are discussions to expand IOSS to include higher value values beyond €150. While, the outcome remains uncertain, we predict there will be a higher threshold for IOSS VAT payment in 2027.

How a Canadian seller registers for IOSS

Non-EU sellers must appoint an IOSS intermediary established in the EU. The intermediary registers on behalf of the Canadian seller in one EU member state, and that single registration covers sales to consumers in all 27 member states. The Canadian seller receives an IOSS VAT identification number (format: IMxxxxxxx) which is provided to the carrier on each shipment.

Jet Worldwide can assist Canadian e-commerce businesses in connecting with IOSS intermediaries and integrating the IOSS number into shipping workflows. Contact our team for IOSS guidance.

How the New Customs Duty Will Be Paid

EU consumers will pay the 3 euro customs duty per item in one of two ways, depending on the terms and conditions of the selling business:

Option 1 — Charged at checkout (DDP / Delivered Duty Paid)

Some websites will be set up to collect the duty at the point of sale.

Option 2 — Charged on delivery (DAP / Delivered at Place)

Other websites may not collect the duty at checkout. In this case, the delivery company (for example, the national postal service or a courier such as FedEx, UPS, or DHL) will require the consumer to pay the 3 euro duty per item before the goods can be delivered. Most carriers also add a disbursement or handling fee (typically 5 to 15 euros) for collecting duty and VAT on behalf of the consumer.

Recommendation for Canadian sellers: Contact our team to explore direct shipping options and dedicated clearance processes.

Impact on Returns and Refunds

The new rules significantly affect the returns process for goods purchased from outside the EU:

- Customs duty is non-refundable: If a consumer returns an item, the 3 euro customs duty will not be refunded, unless the goods are faulty or defective.

- VAT refunds vary by seller: Some online suppliers will refund the VAT paid if an item is returned, but many will not. This depends on how individual businesses account for their VAT liabilities through IOSS or the carrier's import process. This is often not obvious to consumers at the time of purchase.

Implication for Canadian sellers: Your returns policy and terms of service should clearly state whether customs duty and VAT are refundable on returned goods.

CETA and Preferential Origin: When the 3 Euro Duty Does Not Apply

Under the Canada-European Union Comprehensive Economic and Trade Agreement (CETA), most Canadian-origin goods can enter the EU duty-free (0% tariff) when accompanied by a valid origin declaration on the commercial invoice.

However, CETA preferential treatment applies only to H1 (full customs) declarations, not to H7 simplified e-commerce entries.

This creates an important strategic decision for Canadian sellers:

- H7 route (under 150 euros, B2C): The flat 3 euro per item duty applies regardless of Canadian origin. CETA preferences cannot be claimed on an H7 declaration. But the process is simpler, faster, and cheaper per parcel.

- H1 route (any value, B2B or B2C): If the goods are of Canadian origin and you provide a valid CETA origin declaration, the duty rate can be 0%. But the H1 process is more complex, requires a full HS code, and typically involves a customs broker fee.

For most low-value e-commerce shipments, the H7 route with the 3 euro flat duty is more practical and cost-effective than filing an H1 entry with CETA origin documentation. But for higher-value Canadian-made goods (handcrafted products, premium food, specialized equipment), the H1 with CETA 0% duty may save money, especially on multi-item orders where the flat 3 euros per item would otherwise add up.

Read more: Country of origin vs. country of shipment

Shopping Within the EU: Identifying Where Goods Actually Ship From

There is no customs duty if goods are located in an EU country at the time the order is placed. The 3 euro duty applies only to goods shipped from outside the EU.

Some websites may appear as if the business is EU-based — by using a local domain (for example, a ".ie" or ".de" domain), showing prices in euros, or displaying a European return address — but the goods may actually be shipped from a non-EU country such as China, the United Kingdom, or Canada.

For EU consumers: Check the website's "Terms and Conditions" or "About Us" page to confirm the physical business address and the location from which goods will be shipped.

For Canadian sellers: Be transparent about your shipping origin. If you ship from Canada, clearly disclose this and explain any applicable duty and VAT in your checkout flow. Sellers who pre-stock inventory in EU fulfillment warehouses avoid the 3 euro duty entirely because the goods are already inside the EU when the consumer orders.

Action Steps for Canadian E-Commerce Sellers

If you sell online to EU consumers, take these steps before July 1, 2026:

- Register for IOSS (through an EU-based intermediary) to collect VAT at checkout and enable H7 simplified customs filing.

- Update your checkout flow to show the 3 euro per item customs duty to EU buyers. If you use Shopify, WooCommerce, or a similar platform, work with your developer or shipping app to integrate duty calculation.

- Update your terms and conditions and returns policy to state clearly whether customs duty and VAT are refundable on returned goods.

- Decide between DDP and DAP for your EU shipments. DDP (collecting duty and VAT at checkout) is strongly recommended for customer satisfaction.

- Evaluate CETA origin for higher-value shipments. If your products are Canadian-made, the H1 route with a CETA origin declaration may eliminate duty entirely on orders over 150 euros.

- Consider EU fulfillment for high-volume sellers. Pre-stocking inventory in an EU warehouse eliminates the 3 euro duty, speeds delivery, and removes cross-border friction for consumers.

Jet Worldwide supports Canadian e-commerce businesses with IOSS integration, H7 customs filing, and direct delivery solutions across all 27 EU member states. Contact our team to prepare for July 1, 2026.

EU VAT Rates by Member State (2026 Reference)

VAT is charged on top of the 3 euro customs duty. Rates vary by member state. The standard rates for the most common Canadian export destinations are:

| Member State | Standard VAT Rate |

|---|---|

| Germany | 19% |

| France | 20% |

| Netherlands | 21% |

| Spain | 21% |

| Italy | 22% |

| Belgium | 21% |

| Ireland | 23% |

| Poland | 23% |

| Sweden | 25% |

| Hungary | 27% |

Note: Reduced VAT rates apply to certain product categories (books, food, children's clothing) in many member states. Confirm the applicable rate with your IOSS intermediary or customs broker.