There has been a seismic shift in U.S. trade policy. On February 20, 2026, the U.S. Supreme Court ruled 6 to 3 that the International Emergency Economic Powers Act (IEEPA) does not grant the President the authority to impose tariffs. In the world of cross-border logistics, this means sweeping changes for importers, customs brokers, and shippers relying on international trade lanes.

Table of Contents

The government moved swiftly to fill the gap. Beginning February 24, 2026, U.S. Customs and Border Protection (CBP) will stop collecting IEEPA duties as those tariff codes go inactive. In their place, the Administration has pivoted to Section 122 of the Trade Act of 1974.

Read about CAPE refund process effective April 2026 (for IEEPA Duties)

Executive Summary:

Unconstitutional IEEPA tariffs replaced Temporarily by Section 122

Section 122:

- Standard 10% tariff from all origins (Ongoing regarding an increase to 15%)

- Is in addition to - not in lieu of - existing MFN/Column 1 rates

- Authority under this Section expires July 24, 2026 (unlikely Congress will approve and extension)

Between now and July 24:

Expect new tariffs via Sections 301 (Unfair trade) and 232 (National Security)

IEEPA Refund mechanism has not been defined, potential sticking points

- Liquidated entries?

- Informal courier entries where UPS, FedEx and DHL acted as Importer of Record?

- Foreign Importer of Record shipments sent to the USA delivery duty paid via courier?

- Will refunds be via customs (ACE) or via Court of International Trade?

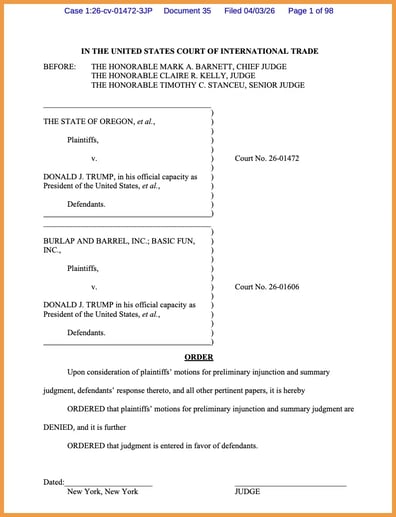

Are Section 122 Tariffs Also Unconstitutional?

Plaintiffs have filed suit challenging the legality of Section 122 tariffs. The filing has been made in the same court used to challenge IEEPA tariffs, The Court of International Trade (CIT). A final ruling either for or against is uncertain, subject to appeal, a likely to occur after the tariffs expire.

1. The End of IEEPA Tariffs

IEEPA was designed as an emergency economic sanctions authority, allowing the U.S. President to regulate commerce after declaring a national emergency regarding foreign threats. It was traditionally used for sanctions, asset freezes, and specific entity restrictions.

The Supreme Court ruled that IEEPA was never written as a broad tariff statute. Using it to bypass Congress violated the separation of powers. As a result, all broad-based tariffs implemented strictly under IEEPA are now invalid.

2. Enter Section 122: Temporary Import Surcharges

Within hours of the Court decision, the White House announced a global import surcharge using Section 122. This tool acts as a short-term bridge rather than a permanent framework.

- Effective Date: February 24, 2026.

- Duration: Up to 150 days (running through July 24, 2026).

- The Rate: The initial proclamation set the rate at 10 percent. However, the President subsequently announced an immediate increase to 15 percent, which is the maximum allowed under this authority. Importers must brace for higher cost structures as entries clear under the new setup.

- Application: This surcharge sits on top of standard Most Favoured Nation (MFN) duties and existing Section 301 measures. It does not stack on Section 232 tariffs. Targeted exclusions exist, such as books and informational materials.

3. Postal vs. Commercial Shipments

This policy direction delivers a major structural signal to the logistics industry: postal and commercial duty treatments are on a clear path toward total alignment.

Beginning February 24, postal shipments will also face the new surcharge. The current Qualified Party model will continue to manage duty collection and remittance to CBP. The surcharge remains until the 150-day window closes or a brand-new postal entry process goes live. This closes the gap between traditional freight and e-commerce postal channels.

4. Sections 301 and 232: What Remains Unchanged

Not all tariffs were struck down. Statutes explicitly delegated by Congress remain completely intact. Understanding these distinct legal lanes is vital for accurate customs declarations.

| Authority | Trigger | Status |

|---|---|---|

| IEEPA | National emergency statute | Struck down by Supreme Court |

| Section 301 (Trade Act of 1974) | Unfair trade practices (e.g., China tariffs) | Active and unchanged |

| Section 232 (Trade Expansion Act of 1962) | National security threats (e.g., steel, aluminum) | Active and unchanged |

Note: The de minimis ban remains in place alongside Section 301 and Section 232 tariffs.

5. Practical Steps for Importers and Brokers

The transition from IEEPA to Section 122 officially begins at midnight on February 23 into February 24. CBP has confirmed they are reviewing the ruling and will issue ACE filer guidance shortly (CSMS #67823350). In the meantime, customs experts suggest the following actions:

- Review Entry Summaries: Watch your entries closely over the coming weeks to optimize duty payments based on the precise termination date of IEEPA tariffs and the start of Section 122.

- Pay During Transition: Legal experts recommend paying the duties until CBP releases official guidance. Importers usually have a 10-day window to correct entries once clarification is published.

- Monitor Refund Opportunities: It is not yet clear how refunds will be handled for liquidated entries outside the 10-day window. This decision will fall to the Court of International Trade (CIT). Importers should monitor liquidations and file protests where applicable.

- Prepare for the Pivot: Because Section 122 is temporary, expect future long-term tariff actions to shift toward Section 301 investigations.

While the Supreme Court ruling removes one layer of tariff policy, the rapid implementation of Section 122 proves that trade volatility continues. Relying on an experienced logistics partner to navigate these structural changes is more critical than ever.

Need Help Navigating the New Customs Landscape?

Our cross-border experts are tracking every regulatory update to keep your supply chain moving.

Contact Our Logistics Team